As I was looking over last month's apartment numbers, I realized there was a term on the financial statement that I never really paid much attention to and that some people might not have a good idea of the meaning of. I thought it might be worth explaining how the income portion of a financial statement is filled out and what each term means.

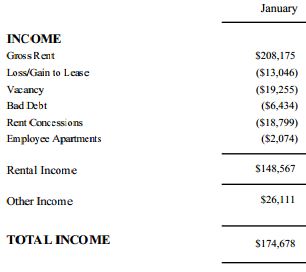

Below is the actual Income portion of the financial statement for the Houston apartment complex for January 2012.

Negative numbers are shown in parenthesis. Let's go over each term.

Gross Rent - This is the amount of rent that would be collected if every unit in the apartment was rented at market rates.

Loss/Gain to Lease - This is the term I figured some people might not know about. Apartments are typically rented out on a 1 year lease. Sometimes longer, sometimes shorter, but typically the tenant signs a contract to pay a certain amount of rent each month for a set number of months. Suppose a tenant signed a lease to pay rent of $500 per month for 1 year and that this is the typical rent for the area at the time of lease signing. Now suppose that after 6 months, due to improvements in the property, a stronger housing market in general, or other factors, the typical rent for a similar apartment in the area rises to $600. At that point, if a new tenant were to rent this apartment, management could charge $600, but since the existing tenant has a contract to pay only $500, the property is losing out on on $100 per month. This is known as "loss to lease" - We've lost $100 in income because the tenant has a 1 year lease preventing us from raising rents. The opposite also applies - if typical rents drop to $400, then we have a "gain to lease" of $100 per month because the tenant is paying $100 more than we could charge a new tenant.

Vacancy - This is pretty obvious. If an apartment is not rented, this is the amount of rent we are losing.

Bad Debt - Income we are owed, but have not been able to collect. For example, if a tenant bounces a check, that rent amount is bad debt (at least until it has been collected).

Rent Concessions - How much we give away in order to get tenants to sign leases. When you see advertisements for apartments that say "First month's rent free!", that is a rent concession and the amount of one month's rent would show up in this category.

Employee Apartments - Managers and / or other building employees sometimes live on site and, in exchange for their services, get either free or discounted rent. This line tracks this amount.

Notice that these amounts, even though they are negative, show up in the Income portion of the financial statement, not the Expenses section. This is because they are not actual amounts we have paid out. They represent

reductions in the

maximum possible income the property can achieve (as given in the first item, Gross Rents). The Expense portion of the financial statement only contains amount we have actually paid out.

So, as an investor, what you want to see when looking at a property's financial statement is the Gross Rent figure rising and the other figures decreasing (or getting closer to zero). In most cases, the monthly Gross Rent is typically assumed to be static for an entire year, even though market rents may vary month to month. This is just to make budgeting, reporting, and forecasting easier. However, if you are able to look at the financial statements of a property for multiple years, look for this number to be rising each year.

Loss / Gain to Lease is something you want to see approaching zero. A positive number ("gain to lease") is nice in the short term, but that would mean most of your leases are at above-market prices. In turn, that means tenants will probably be moving to a cheaper property when their leases are up and it may be hard to attract new tenants. Here is a chart of the monthly loss to lease numbers for my apartment for this year (through November):

Not too bad. Pretty big losses, but at least it's trending in the right direction.

I hope that gives you some insight into how to read the income portion of a financial statement for a rental property.